Insights

Inflation-linked bonds, revisited

Craig Alexander and Liam Donnelly

ANALYSIS: Inflation-linked bonds in high inflation times – good concept but how have they fared?

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how they work and what New Zealand Debt Management (NZDM – the department of the New Zealand Treasury responsible for issuing government debt) was doing to promote and support the inflation-linked bond market.

With almost three recent years of high inflation under our belts, have inflation-linked bonds offered the protection they conceptually should have?

As a brief reminder, these bonds differ from nominal debt securities – which typically pay a fixed interest rate or coupon not adjusted for inflation and are generally the more popular variety of debt instrument.

The theoretical value of an inflation-linked bond is primarily associated with changes in the rate of inflation, which in New Zealand is measured by the Consumers price index (CPI).

Simply put, inflation-linked bonds provide a return that equates to a real yield, a return adjusted for inflation rather than a nominal yield, a return that is a pre-set coupon not adjusted for inflation.

Inflation still front of mind

Since we last wrote on the topic, inflation is still front of mind for investors globally, with financial markets seemingly hanging off of every data release in an attempt to understand where central banks may take interest rates next.

Indeed, our own Reserve Bank of New Zealand has updated its current thinking in a recent speech by its chief economist, Paul Conway, entitled, ‘The path back to low inflation in New Zealand’ on March 23, 2023.

Probably a little late, as the last three published annual CPI prints came in above 7%; for the record, annual inflation hasn’t been within the RBNZ’s target band of 1-3% since March 2021.

To assess the performance of an inflation-linked bond, we need to compare its return with that of an equivalent maturity notional bond.

For this analysis we’ve used the S&P/NZX New Zealand Government 5+ Year Index, which assesses the performance of nominal New Zealand Government bonds with maturity dates greater than five years and the S&P/NZX New Zealand Inflation-Indexed Government Bond Index.

While these two indices are by no means identical, they have a reasonably well-matched duration at 8.8 years and 9.2 years respectively, meaning the two indices should have a similar level of interest rate sensitivity to movements in the risk-free rate.

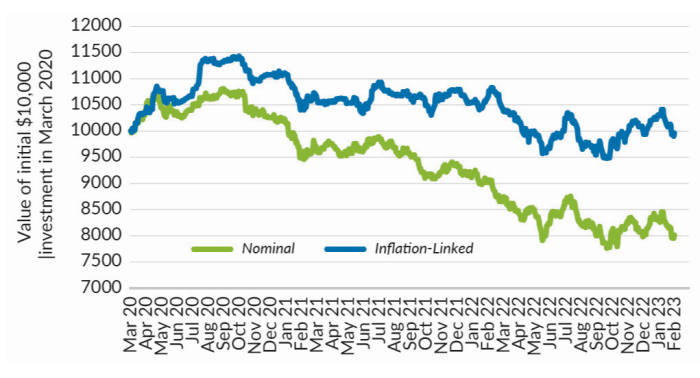

Total return of NZ Govt bond indices

Source: Refinitiv

So, have inflation-linked bonds provided inflation protection?

Figure 1 says yes, at least relative to nominal bonds – the inflation-linked index has clearly outperformed the nominal New Zealand government bond index to the end of February 2023.

The inflation-linked index was essentially flat, losing an annualised -0.14% while the nominal index lost an annualised -7.34% over the same period.

However, the -0.14% annualised return of the inflation linkers was materially below the actual annual rate of CPI inflation between March 2020 and December 2022, which has been closer to +4.25%.

This means that an investor in inflation-linked bonds has suffered a loss in purchasing power from high inflation – but, positively, their investment has done better than the significant loss of the nominal bond equivalent.

Why no better offset?

So, why haven’t inflation-linked bonds better offset the effects of inflation over the shorter term, especially if the value of domestic inflation-linked bonds is reset against the rate of CPI each quarter?

Well, they have, if we extend the observed time horizon to many years, rather than just a few.

New Zealand’s five-year annualised inflation rate was 3.17% to the end of December 2022. The five-year return over the same period for the S&P/NZX New Zealand Inflation-Indexed Government Bond Index was 3.49% which comfortably exceeded the negative return of -0.39% for the S&P/NZX New Zealand Government 5+ Year Index.

In our experience, the short-term performance of New Zealand Government inflation-linked bonds comes down to the perception of where inflation will go over the next year or so.

Currently, the market is backing the RBNZ to stomp inflation back down to its target of around 2%, or the middle of the 1% to 3% band. We can see this is in the assumed inflation break-even rate of the New Zealand Government 2.50% 15/09/2035 inflation-linked bond, which is currently 2.25%.

And in order to observe how quickly the market thinks the RBNZ will bring inflation under control we need to look at the implied inflation break-even rate of the substantially shorter maturity New Zealand Government 2025 2.00% 15/09/2025 inflation-linked bond, which is 3.50%.

Understand the implications

To cut a long story short – the message we’re trying to get across to the interested investor is to better understand what the professional market is implying in the way that it prices the more sophisticated financial products, such as inflation-linked bonds, so as to get some additional insights into the potential performance of wider portfolio returns.

How is this for a starter: Actual inflation for the year to the end of 2022 was 7.20% and, over the next two years, the professional market expects inflation to average 3.50%. Maybe our interest rates are still too low?

Disclaimer: This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. It does not contain financial advice. This article was supplied free to NBR and first published 4 April 2023.